How Can Grandparents through their Estate Plans Provide for their Grandchildren?

Photo by 🇸🇮 Janko Ferlič on Unsplash

Question:

What should grandparents think about in terms of planning for their grandchildren?

Response:

Most grandparents do not plan specifically for their grandchildren. They provide that their estates pass to their children and if any of them predeceases them, that child’s share passes to his children. Some grandparents make relatively small specific bequests directly to their grandchildren. Most wills and trusts contain standard language permitting the personal representative of the estate or the trustee to continue to hold funds in trust until the grandchildren reach a specified age, often 25.

But there are a number of steps grandparents can take on behalf of their grandchildren. Here are a few:

Family Protection Trust

I’m a proponent of what we call a “family protection trust.” Under traditional trust law, a trust created by someone else can be drafted to protect the assets it holds in the event of divorce, from creditors, and from having to be spent down if the beneficiary needs public benefits. So, rather than having your estate distributed outright to your children and grandchildren, you can have it go in trust for their benefit with the protections described above. Then the funds can be set aside as something like insurance in case they are ever needed, rather than being commingled with your children’s own funds and subject to claim in the event of unfortunate circumstances. Such trusts also keep the funds in the family in the event a child dies early, rather than passing to the surviving spouse and perhaps going to a new family if he or she remarries.

Grandchildren’s Trust

Some grandparents create a special trust for their grandchildren as a group for a number of reasons. This way, the grandchildren don’t have to wait until their parents pass away to receive an inheritance from their grandparents. Grandparents are more likely to take this step in two somewhat opposite circumstances. In the first, their children don’t need their funds since they’re doing well financially on their own. Second, the grandparents may not trust the parents to take adequate care of the grandchildren or they may have a difference of opinion on how freely they should be supported.

Often these trusts are created for specific purposes, such as to provide for educational costs, for travel, and for health care emergencies as necessary, all depending on the grandparents’ goals and values. They often treat the grandchildren as a group, leaving it up to the trustee to determine how to disburse funds, rather than creating separate shares for each grandchild. This can make it easier to manage the funds and treats all the grandchildren equally.

If you create a grandchildren’s trust, it’s up to you what portion of your estate to fund it with, whether a percentage or a specific dollar amount. I’m a fan of funding it with a child’s share of the estate. Here’s how that works: If you have two children, you would divide your estate three ways, with one share each going to your children and one share to the grandchildren’s trust. If you have three children, you would divide your estate four ways, with a quarter going to each of your children and a quarter going to the grandchildren’s trust. And so on.

Use of the grandchildren’s trust can satisfy some of the purposes of family protection trusts without tying up assets for the next generation. In order for family protection trusts to work, they must limit the next generation’s access to the funds they hold. Some children object to those restrictions, arguing that they can well manage their own funds and that it’s demeaning to have to ask a trustee for funds. So, one solution is to give them their share of your estate outright, but to set some funds aside for the following generation through a grandchildren’s trust.

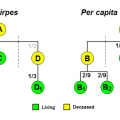

Per Capita vs. Per Stirpes

In terms of treating grandchildren equally, you have the choice of having your will or trust distribute funds “per capita at each generation” or “per stirpes.” This distinction only matters if two or more of your children were to die before you or to die before a trust for their benefit was completely distributed. The best way to explain these two terms is by example.

Let’s assume you have three children and six grandchildren distributed as follows:

Child A – one child

Child B – two children

Child C – three children

Let’s also assume that your estate when you pass away is valued at $900,000. If all of your children were to survive you, they would each receive $300,000. If one of your children were to die before you, her child or children would receive her $300,000 share to be divided among them. But what happens if two of your children were to die before you, let’s assume Child A and Child C?

Here’s where the distinction between per stirpes and per capita at each generation would come in to play. Under the per stirpes approach, which was traditional until recently, each child would still get his parent’s share. So the one child of Child A would receive $300,000 and the three children of Child C would each receive $100,000. The more modern per capita approach provides that the two shares be combined and that all children of the predeceased members of the first generation share equally. In this case, the four children of Child A and Child C would each receive $150,000 ($600,000/4 = $150,000).

Our firm has adopted the per capita approach as the default unless our clients prefer per stirpes, but it’s up to you which way you want to go.

Related Articles:

Using Third-Party Trusts for Asset Protection

What is the Difference Between Per Stirpes and Per Capita Distribution?

Related Articles

Putting off planning your estate?

Don’t know where to start?

This simple-yet-comprehensive guide provides everything you need to know (in plain English).

Don’t know how your trust works?

Whether you’re creating a plan, managing a trust, or are a beneficiary of a trust, this book is your easy-to-read roadmap.

I like the idea of a family protection trust but who does one designate as the trustee for each adult child? If they are their own trustee then what prevents them from comingling assets with their spouse? Is a corporate trustee the only alternative then?

Fred,

An independent trustee, whether corporate or a trusted individual, is the best option in terms of asset protection. But many clients don’t want to pay professional trustee fees and are put off by the impersonal nature of such trustees. In our family protection trusts we often follow a middle route. We name the adult child as trustee of his or her own trust, but only for purposes of managing the trust assets and withdrawing income. If the adult child wants principal distributions he or she must name an independent trustee at that time. This works on paper. It’s weakness is that it depends on the adult child beneficiary following the rules of the trust. If he or she breaks those rules, for instance making a principal withdrawal, the trust loses its protection from creditors and in the event of divorce. We explain this to clients and allow them to make the choice as to who should serve as trustee.

Harry